By Anisa Pinatih

This commentary looks at how the disruptions caused by COVID-19 has impacted the economy in general and the construction sector in particular; how governments are assisting workers to wade through the difficult times; and how, in some cases, measures are not delivered in the best ways possible so that workers, who are already vulnerable in normal situations, are put in an even more disadvantageous position.

Impacts on the macroeconomy

Generally, as lockdown measures to suppress the transmission continue, the global economy will also continue to plunge into a recession. Supply chains are hurt, sectors collapse and enterprises stop operations, resulting in workers facing unemployment and the loss of income.

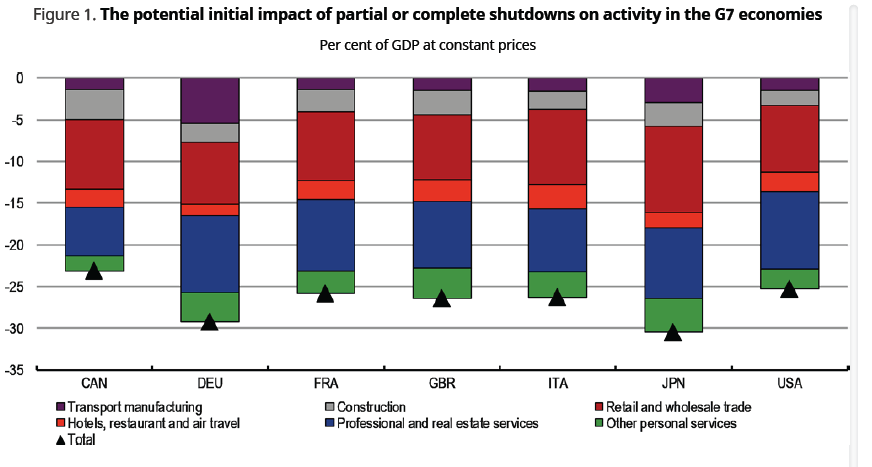

SECTORAL IMPACTS OF THE WIDESPREAD SHUTDOWN

OECD’s initial evaluations of the economic impacts vary from sector to sector. Within service sectors, travel and tourism, and any sectors involving direct contact between consumers and service providers, are massively impacted. Non-essential construction work is also being negatively affected, either because of movement control affecting labour availability or because of temporary reductions in investment. The overall direct initial hit to the level of GDP is estimated to fall between 20 to 25 per cent in G7 economies. The impact on annual GDP growth would depend on how long these measures remain in place. If the advanced economies are taking such a hard hit, the developing countries will suffer even more.

It is also important to note that construction sector is developing more rapidly and takes up a higher share in GDP in developing countries than those in G7 countries, so the outlook in many Southeast Asian countries might not be as positive as the report by OECD.

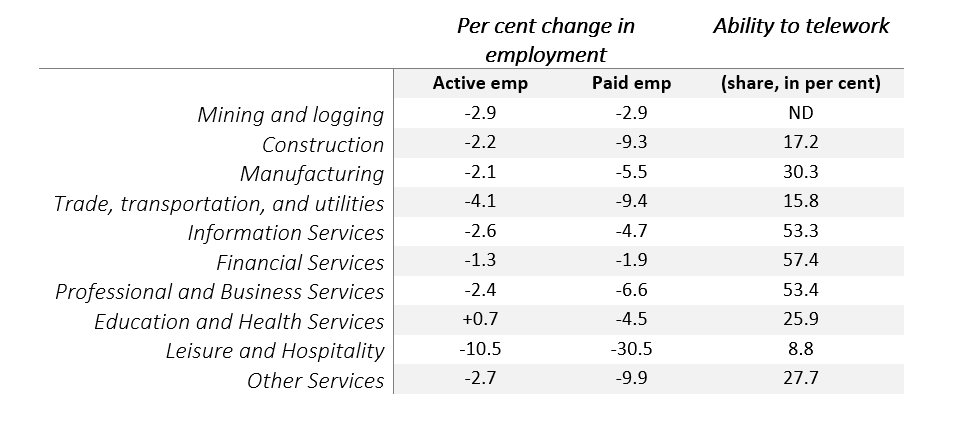

THE GENERAL ABILITY TO TELEWORK

In terms of paid employment, another research report points out that, in absolute terms, the most significant decreases were, in their respective order: in leisure and hospitality; trade, transportation, and utilities; professional and business services; education and health; manufacturing; and construction. In relative terms, the largest employment losses were in leisure and hospitality (30.5 per cent); other services (9.9 per cent); trade; transportation; and utilities (9.4 per cent); and construction (9.3 per cent). It appears that the largest employment losses occurred in sectors with low general ability to telework. Construction industry, unfortunately, is not among those with the highest ability to work from home.

Table 1. Cumulative Employment Changes and Ability to Telework (Source: Tracking Labour Market Developments during the COVID-19 Pandemic: A Preliminary Assessment)

BIGGER THAN THE SARS OUTBREAK

Studies of the macroeconomic effects of the SARS pandemic in 2003 found negative effects on economies because of the significant decline in the consumption of goods and services, and an increase in operation costs. Although SARS resulted in lower number of cases and deaths, the global impacts were substantial and not limited to the directly affected countries. By the time the SARS outbreak was under control, there was a 0.5 to 1 per cent point reduction in China’s economy, with the cost to the global economy estimated to have had been USD54 billion (China Center for Economic Research).

The economic impacts COVID-19 is likely to be way more detrimental than that. A researcher at IESE Business School points out that in 2003, China made up 3 per cent of the global economy, but now it is above 16 per cent. Any shock to the Chinese economy will have a spillover effect on global markets in all different sectors. Also, the global economy is much more integrated than it was 15 years ago, so economic disruption in one location will have much larger impacts on others. In 2003, China’s 1-per cent economic decline might not be noticeable, but now the recession will have a greater ripple effect.

THE IMPACT ON CONSTRUCTION SECTOR

Construction sector might not be the hardest hit, compared to say tourism and service sectors, but it is important to note that resiliency depends on the ability to telework. If the COVID-19 pandemic drags on and lockdowns continue, it is likely that the sector will experience a more significant downturn. Also, the spillover effects from China will be greater this time. Many construction materials are imported from China. The world shipping companies are dominated by China. Any disruptions to the production and supply chains will surely negatively affect progress on any project.

With the high shares in the global economy, any disruptions to the Chinese economy will have a great spillover impact on global markets in all different sectors, including those in Southeast Asian countries.

Governments’ assistance for workers

To minimise the impacts on workers, tripartite partners—employers, unions and workers, and the government—have developed guidelines to give timely guidance to employers on sustaining their businesses and saving jobs. Summarising from the Country Policy Responses by International Labour Organisation (ILO), below are some of the policies:

SINGAPORE

The Government of Singapore supports individuals by giving social protection in various scales to almost everyone—tripled grocery vouchers; cash pay-out for all adults; cash for household needs for lower-wage workers; for self-employed persons; for taxi drivers; the elderly; and the unemployed. Employment retention is encouraged even if that means a short-period arrangement. In case of temporary lay-offs, employers must pay 50 per cent of the gross salary.

In protecting workers, apart from the social distancing order and work from home arrangements, the Ministry of Manpower provides temporary housing and access to healthcare; and encourage employers to pay employees with stay-at-home notices.

Some buildings that have become hotspots of the outbreak, such as those where foreign workers reside are declared as isolation areas to control the transmission. Some of the key governmental measures to control the spread is by strictly regulating the spatial use.

Also read: Handling COVID-19 in Singapore: Government Mitigation and Regulation on Spatial Use

April 2020: Migrant workers’ dormitory, S11 Punggol, where the largest cluster of outbreak was found; image by kandl/Shutterstock

INDONESIA

Fiscal policy for workers in Indonesia covers, among many others, social protection budget of up to IDR110 trillion (USD5.5 billion); tax incentives; expansion of conditional cash transfer programme and staple food programme; electricity bill discount for three months; and six-month tax exemption for workers with an annual income below IDR200 million (USD13,500).

Social assistance is provided to those who are laid off due to the outbreak—a cash compensation in the amount IDR1 million (USD67.5) per month up to three months. The Ministry of Manpower also recommends the remission of Employment BPJS (national insurance) fee contributions to companies affected by COVID-19 for up to six months.

The ministry requests employers to discuss in advance with the trade unions/workers representatives at the company level and take alternative measures before laying off workers, such as by reducing wages and perks of the top-level positions; reducing work shifts; limiting/removing overtime work; reducing work hours/workdays; and opting for temporary lay-off or rotational work.

MALAYSIA

The Malaysian government provides RM50 billion (USD11 billion) as guarantee scheme for the purpose of financing working capital requirements for viable businesses in all sectors facing difficulties due to COVID-19. To support individual workers, financial assistance is provided to identified target groups.

For any worker infected by the virus, one-off cash schemes will be rolled out regardless of the sector (private, government-scheme plantation, or government offices) and their contract status (permanent or contract). Eligible individuals are also allowed pre-retirement withdrawals of up to RM1,500 (USD350). A tiered discount for electricity bills with rates ranging between 15 and 50 per cent are introduced too.

Payment of salaries and extension of contract of public-contract services workers are mandatory. There is also a subsidy programme to assist employers in retaining their workers of up to RM13.8 billion (USD3.1 billion). The government will provide salaries of up to three months, depending on the size of enterprise and the number of workers. For employers who choose to receive this assistance, they will be required to retain their employees for at least six months.

Oftentimes, there are gaps between policy and practice which are particularly disadvantageous for workers, including unfair job termination, unpaid leave, and higher risk of infection due to non-ideal living spaces.

Gaps between policy and practice

The governments may have done everything in their power to help workers, but like any other measures, especially during a crisis, there are always gaps between policy and practice. These are particularly disadvantageous for migrant workers, contact-based workers, or any blue-collar workers with little to no financial cushion.

NON-IDEAL LIVING SPACES: IMPOSSIBLE FOR SOCIAL DISTANCING

Migrant dormitories in Singapore became the hotspots of the virus spread—the S11 Punggol; the Westlite in Toh Guan; and a dormitory in Sungei Kadut. Most of the affected workers were Indian and Bangladeshi men.

A report by Transient Workers Count Too mentioned that the dorm conditions are highly susceptible to infection as 12 to 20 men were housed in one room with double-decker beds. At the 18-storey main block of Westlite in Toh Guan, each room housed between 10 and 20 workers. Needless to say, adopting government measures in such spaces was almost impossible. Safe distancing in common areas will not be effective if workers are crammed into small dorm rooms and use packed lifts.

Dormitory operators packed them in because they have to, given the high cost of land in Singapore, and because they could, by taking advantage of a loophole in the regulation, which requires a minimum of 4.5-square metre gross floor area (GFA) of living space per worker. The math is simple: the room is 12 metres times 7.5 metres, which makes 90 square metres, equivalent to 4.5 square metres per person. With this, it was not wrong to say that the government requirement had been met. But the real condition was far from ideal.

A mass transfer of workers is not something that dormitory operators can organise on their own. Poor planning and organisation of workers relocation might even increase transmission risk of the virus amongst the wider community.

Construction is one of the 10 sectors that remain operational during the Large-Scale Social Restrictions (PSBB) in Jakarta; image by ardiweb/Shutterstock

Meanwhile in Jakarta, reported by Berita Satu, construction workers are instructed to live on-site during the Large-Scale Social Restrictions (PSBB) order. The construction industry is among the 10 sectors that remain operational during the 14-day PSBB order. The employers are encouraged to provide shelters, amenities, meals, health facilities; as well as to adhere to the social distancing rules. But anyone who is familiar with construction site conditions will be able to imagine how hard this would be.

In Malaysia, a report published by ILO mentioned that concerns are also mounting about the spread of the virus in crowded immigration detention centres and in migrant workers’ housing. On 2 May 2020, a cluster of 28 infections was reported among migrant workers in a construction site. Previously, on 10 April 2020, a cluster of 79 infections was also identified in three building housing migrant workers—Selangor Mansion; Malayan Mansion; and Menara City One in central Kuala Lumpur.

JOB TERMINATION AND UNPAID LEAVE

The resilience of Indonesian construction companies is starting to shake, and decision makers have started to think about the worst-case-scenario in dealing with the impact of COVID-19. Budi Harto, President Director of PT Adhi Karya Tbk (ADHI), a state-own construction company, as reported by CNBC Indonesia, said that they are only able to finance construction workers for the next three months.

ADHI seeks not to terminate employment for workers and employees even if the situation continues to deteriorate in the next three months. However, if the crisis continues for more than six or nine months, it is likely that ADHI will not work on any projects, but again, laying off workers will be highly avoided.

To prevent more job terminations in Jakarta, the government was expected to roll out more extensive measures, such as by reducing production costs or introducing a rotational policy.

But such endeavours will be difficult to undertake as the economy is plunging deeper. Jakarta Post reported that thousands of workers have been laid off already, or forced to take unpaid leave, with the number reaching 162,416 in the capital as more than 18,000 companies are taking a hard hit. The report further mentions that as per 5 April 2020, a total of 30,137 workers have been terminated by 3,348 companies, while another 132,279 employees have been sent home without pay.

The Confederation of Indonesian Trade Unions (KSPI) president, Said Iqbal, pledged the government to roll out more extensive measures to anticipate more layoffs; and encouraged companies to reduce production costs by giving more days off to workers or roll out a rotational policy to continue production.

MIGRANT WORKERS: TERMINATED FIRST?

The Movement Control Order (MCO) in Malaysia has undoubtedly impacted the migrant workers, putting at risk those who are unable to work during the MCO and those who continue to work in essential services. The economic impact of the MCO is expected to be substantive. The Ministry of Human Resource, as reported by ILO, has advised that if lay-offs are inevitable, foreign employees should be terminated first.

In the case of migrant workers, especially during a crisis, the risk is extremely high, not just in terms of unfair termination. ILO also claimed that there have been reports related to unfair wages; poor living conditions; continuing working in jobs that are non-essential; and uncertainty about employment status due to limited contact with employers. Such specific cases have been followed up and complaints have been filed to the relevant authorities for investigation.

Preventing more detrimental impacts

The direct and indirect impacts of COVID-19 are inevitable and these may even get worse in the second half of the year. Most countries are two to three months behind China, both in terms of the outbreak onset and the implementation of corrective measures. If lockdowns and China’s economy spillover effects continue to drag on, global economic recovery will require extensive measures and efforts. Construction sector, by far, is not among the hardest-hit yet, but industry players must remain cautious and continue to carry out best practices.

Blue-collar workers are likely to suffer the most so governments must pay special attention to them. This is not only for the sake of their well-being, but also for the economy in general. ILO argues that if policy measures to mitigate the impact on the labour market are insufficient, there will be a further round of contractionary effects on economic activity due to lower levels of income and purchasing power among workers. Lower purchasing power means lower consumption, which means lower levels of investment by businesses. In the end, this may result in a deep prolonged recession and wider social inequalities.

– Construction+ Online

Disclaimer: Construction+ makes reasonable efforts to present accurate and reliable information on this website, but the information is not intended to provide specific advice about individual legal, business, or other matters, and it is not a substitute for readers’ independent research and evaluation of any issue. If specific legal or other expert advice is required or desired, the services of an appropriate, competent professional should be sought. Construction+ makes no representations of any kind and disclaims all expressed, implied, statutory or other warranties of any kind, including, without limitation, any warranties of accuracy and timeliness of the measures and regulations; and the completeness of the projects mentioned in the articles. All measures, regulations and projects are accurate as of the date of publication; for further information, please refer to the sources cited.

Hyperlinks are not endorsements: Construction+ is in the business of promoting the interests of its readers as a whole and does not promote or endorse references to specific products, services or third-party content providers; nor are such links or references any indication that Construction+ has received specific authorisation to provide these links or references. Rather, the links on this website to other sites are provided solely to acknowledge them as content sources and as a convenient resource to readers of Construction+.