26 January 2022, Singapore – The Building and Construction Authority (BCA) projects the total construction demand (i.e. the value of construction contracts to be awarded) in 2022 to be between S$27 billion and S$32 billion.

The public sector is expected to contribute about 60 per cent of the total construction demand, between S$16 billion and S$19 billion. This is supported by the strong pipeline of public housing projects including those under the Home Improvement Programme, as well as healthcare developments and infrastructure works such as the Cross Island MRT Line (Phase 1).

The private sector construction demand is anticipated to reach between S$11 billion and S$13 billion in 2022, comparable with the volume in 2021. Given the latest property cooling measures, residential building demand is anticipated to moderate year-on-year amid more cautious market sentiments. However, commercial building demand is expected to increase as hotels and attractions undergo refurbishment to prepare for inbound tourism revival, and older commercial premises are earmarked for redevelopment to enhance their asset values. In addition, the private sector industrial building demand is expected to see some support from the construction of energy storage facilities and biopharmaceutical manufacturing plants. Preliminary Actual Construction Demand in 2021 4. The preliminary total construction demand for 2021 increased by 42 percent to about S$30 billion compared to the preceding year, largely driven by public housing 2 and infrastructure projects as well as an improvement in investment sentiments.

This was about 7 per cent higher than the upper bound of BCA’s earlier forecast of S$23 billion to S$28 billion, mainly due to increase in tender prices resulting from manpower and materials cost inflation. 5. The public sector construction demand increased from S$12.2 billion in 2020 to S$18.2 billion in 2021, underpinned by major projects such as the Cross Island MRT Line, Jurong Region MRT Line, Tuas Water Reclamation Plant and new Build-To[1]Order (BTO) units. Likewise, the private sector construction demand expanded from S$8.9 billion in 2020 to S$11.8 billion in 2021, supported by higher demand for residential, commercial and industrial building developments as the economy recovers.

Forecast for 2023 to 2026

Over the medium-term, BCA expects the total construction demand to reach between S$25 billion and S$32 billion per year from 2023 to 20261. The public sector is expected to lead the demand and contribute S$14 billion to S$18 billion per year from 2023 to 2026, with about half of the demand coming from building projects and civil engineering works.

Besides public housing developments, there are also various major developments in the pipeline, such as MRT projects including the Cross Island Line (Phases 2 & 3) and its Punggol Extension and the Downtown Line Extension to Sungei Kadut, the Toa Payoh Integrated Development, redevelopment of Alexandra hospital and a new integrated hospital at Bedok.

The private sector construction demand is projected to remain steady over the medium-term, reaching about S$11 billion to S$14 billion per year from 2023 to 2026, in view of healthy investment appetite amid Singapore’s strong economic fundamentals.

1 The projection excludes Changi Airport Terminal 5 development and its associated infrastructure projects as well as the expansion of the two Integrated Resorts due to the uncertainty of the global pandemic that could affect construction schedules of such large projects

Construction Output

The total nominal construction output (value of certified progress payments) is projected to increase to S$29 billion to S$32 billion for 2022, from the preliminary estimate of about S$26 billion for 2021. The is due to a steady level of construction demand and the backlog of remaining workloads that were affected by the COVID-19 pandemic since 2020

Singapore Construction Starts

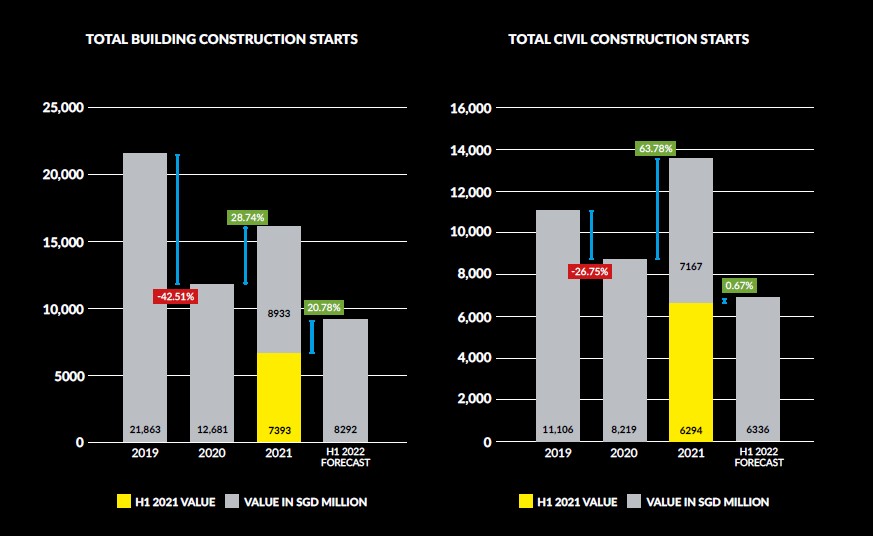

The construction industry in Singapore has been bouncing back in 2021, thanks to government programmes that support the industry, and the restarting of construction works delayed in 2020. The expansion is at 42.52 per cent or SGD29,787 million (from SGD20,901 million in the previous year). This is also made more pronounced by the low base in 2020 when the COVID-19 transmissions started to peak again. While building commencements are seeing a hearty increase of 28.74 per cent to SGD16,326 million in the yearly comparison in 2021, it is the civil that is seeing a more robust annual rise at 63.78 per cent to SGD13,461 million.

The transport sector is one of the government’s priorities to help bolster the recovery and support economic growth in the years to come. Some of the essential contracts are the Jurong Region MRT Line and the Cross Island MRT Line. The disruptions in the construction industry caused by the pandemic mainly contributed to the overall decline in commencements at 37.20 per cent or an estimated SGD20,901 million in 2020.

Workforce shortages, supply chain interruptions and rising materials prices are some of the most pressing concerns that have constrained the industry’s development. To alleviate the pressure, the government has provided support in the form of initiatives such as the Construction Support Package and Extension of Time (EoT) for eligible construction projects; skills certification scheme for foreign workers in Singapore; and the co-sharing of costs and losses brought on by the pandemic or the measures taken. Looking ahead into 2022, it appears that the momentum of construction starts is maintained as seen from a year-on-year rise of 11.53 per cent for the first half of the year.

The building sector is seen leading the charge into 2022, with commencements poised to rise by 20.78 per cent to SGD8,929 million in the year-on-year comparison. The office, health, residential, industrial and education sectors are forecast to maintain a positive year-on-year change in the first half of 2022. Investments in those sectors are sustained due to the gradual return of optimism in the market as COVID-19 vaccination rates increase, and restrictions are eased.

Malaysia Construction Starts

The construction industry in Malaysia has been wading through COVID-19 and all the disruptions it has brought. Construction commencements declined by 19.39 per cent to 58.28 per cent in 2020. Nationwide lockdowns were imposed, allowing only critical construction work during the strictest implementation of the Movement Control Order (MCO). Some of the interruptions or additional protocols were acquiring a new permit to operate and close construction sites.

Adding to the pressure were the rising costs of building materials, especially iron, and workforce shortages. Several initiatives that centre on infrastructure, renewable energy and telecommunications have supported the projections for 2021 and beyond. Total construction starts for 2021 are estimated to have a 16.43 per cent increase year-on-year, reaching MYR67,855 million. The contribution of the building sector leads this with over 60 per cent of the total value at MYR45,176 million. While there is less civil sector input, the segment is projected to register a 48.50 per cent year-on-year change amounting to MYR22,680 million.

In Malaysia’s Budget 2021, the emphasis was given to public infrastructure developments that would bring about more opportunities as these extend to different sectors of the economy and become catalysts for growth. The Jalinan Digital Negara (JENDELA) project that plans to provide better connectivity quality and service is a crucial telecommunications development to watch out for. In line with boosting renewable energy sources, the Large-Scale Solar (LSS) programme continues with LSS 4, adding to a list of significant projects. Likewise, investments from the private sector, including foreign direct investments, propel the construction industry’s prospects with projects such as the SK Nexilis Copper Foil Factory at KKIP IZ 9. Home to several economic corridors, Malaysia promotes its development and amass significant investments from these areas.

The residential sector is seen to perform with a 6.08 per cent increase to MYR22,628 million in 2021 and a decline by 1.67 per cent in the first half of 2022 as concerns with the supply overhang linger. Meanwhile, industrial is projected to continue on a positive trajectory in 2021 until the first half of 2022, partly due to strengthening capacities. The forecast is projected to be at MYR33,708 million, a 6.65 per cent rise compared to the same period in the previous year. Despite a subdued performance throughout 2021, optimism is seen in retail, hospitality and office commercial sectors in the first half of 2022 as vaccination rates increase and restrictions are lifted.

Source: Building and Construction Authority (BCA) with Construction Starts input by BCI Central