YY Lau serves as the Country Head of JLL Property Services (Malaysia) Sdn Bhd with around 20 years of experience in real estate career. She is responsible for the corporate real estate, research and consultancy and agency/brokerage operations in Malaysia. Veena Loh heads the Research and Consultancy Department at JLL. She has also advised on various projects within Malaysia such as Branded Residential Market and Feasibility Study in KLCC and best use for an integrated future TOD in Shah Alam.

With the movement control order (MCO) and work-from-home arrangements that have been put in place for more than a year, the question is whether or not demands for office spaces will rebound. YY Lau and Veena Loh shared with Construction+ their insights on the matter, as well as the property market and outlook for logistics and industrial spaces.

Read: Outlook for industrial and office sectors in 2021 economic recovery

Will prices of decentralised and business park office assets stay firmer than prices of CBD office assets?

Prices of office assets are underpinned by the rents that they are likely to command. Traditionally, the central business district (CBD) office will continue to command higher rents, especially the new ones. However, there may be situations where some well-located and well-connected decentralised offices and offices in the KL Fringe that are very resilient despite the market challenges that may not need to lower their rents as much because they are already comfortably at close to full occupancy. For businesses that require a larger workforce and a larger office space, the decentralised offices and fringes of KL appear suitably located to attract and retain talent, where the offices are sited closer to suburbs where the staff may be staying, thereby offer work-life balance.

Currently, there may be more pressure on rents in KL City due to the significant new supply of prime offices coming up in the CBD. As a consequence of the spike in new supply, a higher overall KLC vacancy is likely to be the case in the short term as it takes a number of years for the market to fully absorb the office space.

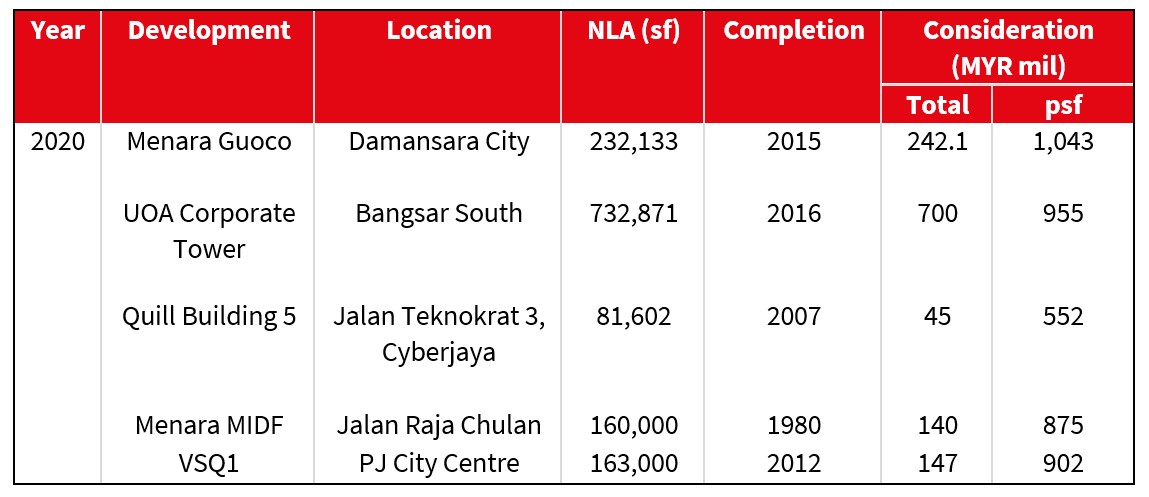

Transaction-wise in 2020, four buildings in KL Fringe and decentralised areas were transacted as opposed to only one in the city centre in 2020. The price of an office building is dependent on many factors including location, connectivity, and integration with other components like retail, etc. whether it is part of a transit-oriented development, age of the buildings, yield etc. With high occupancy and good rentals, prices of office assets are likely to stay firm irrespective of whether it is in CBD or decentralised areas.

Will demand for logistics and industrial space and office space remain high?

Will demand for logistics and industrial space and office space remain high?

Yes, currently the demand for e-commerce and 3PLs [third-party logistics] in Klang Valley is strong. In Penang, the E&E [electricals and electronics] industry is driving the demand for industrial space. In Johor, the demand drivers for logistics and industrial space are from the furniture manufacturing and electronic manufacturer services. Both are doing well due to the geopolitical tensions and tariffs imposed in the US on imports from China. At the same time, there are more orders for better furniture as people are working from home, and require desks and chairs.

The paper and pulp industry is also upbeat as industrialists turn to eco-friendly options for packaging using imported waste paper which is relatively inexpensive at the moment. Glove and medical-related manufacturing and equipment companies are expanding with the spread of the highly contagious COVID-19 and the necessity for precaution and prevention.

Will occupiers continue to demand shorter and more flexible leases?

This depends entirely on the type of occupier and the industry. Start-ups and companies in transition prefer shorter and more flexible leases. There can be MNCs [multinational companies] working on specific projects with a known timeline that may need additional space that their existing building does not have and flexible leases can offer a good option. There are also firms who are using shorter and flexible leases for Business Continuity Plan to ensure that there is a back-up plan for staff to continue operations should the firm is impacted by the COVID-19.

On office space, some companies that may be thinking of expanding and are unsure of expanding into permanent space may consider shifting to flexible space. While this may be true, the offices are generally undergoing an increase in supply when demand has generally shrunk, thereby, resulting in a rise in vacancy rate. Financial institutions prefer longer lease such as six years, whereby they can amortise their capex.

Finally, what are the key trends in the property market and outlook in 2021?

Transaction-wise, there seems to be more listing this year compared to last year, with more sellers out in the market in 2021 while buyers remain cautious. Generally speaking, we hear of less foreign buyers in the market due to the border restriction.

The outlook for industrial, logistics and datacentres are good but for other sectors remain dim for a few reasons. Given the economic slowdown, while new supply has been postponed, the current level of oversupply has yet to be fully absorbed by the market. The uncertain outlook remains—both locally and globally—as a consequence of continued closure of borders. Repeated waves of infection continue and the nearest solution for the national immunisation programme will take at least a whole year to be fully rolled out. All these are keeping investors away from hotels and retail and these sectors are most dependent on tourist arrivals and spending. There are buyers but generally speaking this is for those who know the market well especially operators.

Developers are interested in buying land but their objectives may have shifted more towards looking at developing industrial, data centres and logistic parks. Even REIT [real estate investments trust] companies that are non-industrial are now looking into industrial parks.

– Construction+ Online